Are you dreaming of driving off the lot in a shiny new car? Before you start imagining the wind in your hair and the open road ahead, there’s an important number you need to consider—your credit score.

This little three-digit number plays a big role in determining whether you’ll drive away with the keys or keep waiting at the bus stop. But what exactly is a good credit score to buy a car? Understanding this can be the key to unlocking not only better loan rates but also peace of mind.

Dive into this article to discover how your credit score can impact your car-buying journey, and learn what steps you can take to improve it. Knowing the right score could mean the difference between a sweet deal and a sour one. Ready to rev up your credit knowledge? Let’s get started!

Credit Score Basics

Your credit score is a critical factor in buying a car. It affects the interest rate on your auto loan. Let’s explore the basics of credit scores.

What Is A Credit Score?

A credit score is a number that shows your creditworthiness. It reflects your financial behavior. Lenders use it to decide if they should give you a loan.

How Is A Credit Score Calculated?

Several factors influence your credit score. Payment history is one key factor. It shows if you pay bills on time. Amounts owed are also important. High balances can lower your score.

Different Credit Score Ranges

Scores usually range from 300 to 850. A score above 700 is considered good. A score below 600 may be risky for lenders.

Why Do Credit Scores Matter?

A good credit score can lead to better loan terms. It often means lower interest rates. This can save you money over time.

Paying bills on time can boost your score. Keeping balances low also helps. Regularly checking your credit report is wise. It ensures all information is correct.

Importance Of Credit Score For Car Buying

Understanding the importance of your credit score when buying a car can save you from unexpected surprises. A good credit score can open doors to better financing options, lower interest rates, and potentially more favorable loan terms. But why exactly does your credit score matter so much in this process?

What Is A Credit Score?

Your credit score is a numerical representation of your creditworthiness. Ranging from 300 to 850, it tells lenders how likely you are to repay borrowed money. A higher score suggests that you’re a reliable borrower, which can make you more appealing to lenders.

Impact On Interest Rates

A better credit score often leads to lower interest rates on your car loan. Consider two people buying the same car: one with a score of 750 and the other with 600. The person with the higher score might get a significantly lower interest rate, saving thousands over the life of the loan.

Loan Approval Likelihood

Your credit score plays a critical role in whether you get approved for a car loan. Lenders view a higher score as a lower risk, increasing your chances of approval. If your score is on the lower side, you might face more rejections or be offered less favorable terms.

Negotiating Power

With a strong credit score, you hold more power at the negotiating table. You can shop around for the best deals and use your score as leverage. This can make the car buying experience more favorable for you.

Personal Experience Insight

Imagine walking into a dealership with a high credit score. The confidence in knowing you can secure a good deal is empowering. This advantage can make the car buying process less stressful and more enjoyable.

Have you checked your credit score recently? Knowing where you stand can be the first step in preparing for your next car purchase. Don’t let an unexpected score catch you off guard when you’re ready to make your move.

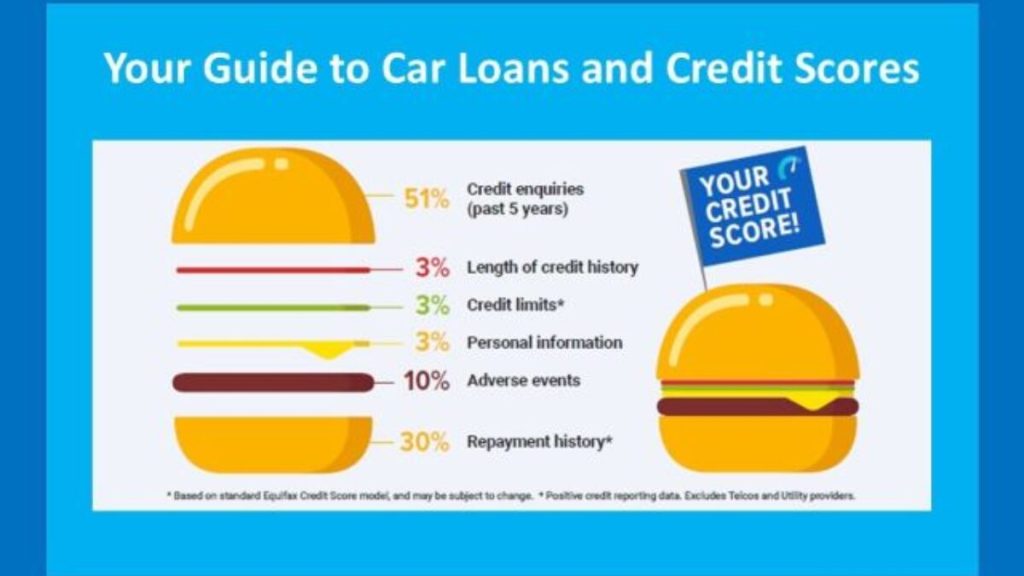

Factors Influencing Credit Scores

Understanding credit scores is crucial when buying a car. A good credit score, typically above 660, can help secure better loan terms. Factors like payment history, credit utilization, and length of credit history influence these scores.

Buying a car is a significant decision, and having a good credit score can make the process smoother and more affordable. But what determines your credit score? Several factors influence it, and understanding these can help you manage and improve your score effectively. Let’s break down the key elements that play a crucial role in shaping your credit score.Payment History

Your payment history is a vital component of your credit score. It’s the record of whether you’ve paid your past credit accounts on time. Lenders want to see that you can manage your payments responsibly. Missed or late payments can significantly impact your score. Imagine the relief of knowing your consistent payment habits are building your credibility! Have you ever checked your payment history for errors? It’s worth doing to ensure accuracy.Credit Utilization

Credit utilization refers to the amount of credit you are using compared to your total credit limit. Keeping your utilization low is crucial. Aim to use less than 30% of your available credit. It’s like having a safety buffer—showing lenders you’re not over-relying on credit. Do you monitor your credit card balances regularly? It’s a simple step that can make a big difference.Length Of Credit History

The length of your credit history can also affect your score. A longer credit history often indicates reliability, as it shows a track record of managing credit over time. Think about how your oldest credit account is helping you. Do you remember when you first started using credit? Keeping older accounts open can be beneficial.New Credit Inquiries

Every time you apply for new credit, an inquiry is recorded on your report. Multiple inquiries in a short period can lower your score. It suggests you might be taking on too much new debt. Have you ever wondered how often you should be applying for new credit? Being strategic with your applications can protect your score. Understanding these factors gives you the power to actively manage your credit score. It’s not just about numbers; it’s about making informed choices that reflect your financial habits. What steps will you take today to ensure your credit score is ready for your next car purchase?Credit Score Ranges Explained

Understanding credit score ranges is essential for buying a car. Your credit score can impact the interest rates you receive. It can also determine the loan terms you qualify for. Let’s break down the credit score ranges to see what they mean for your car buying journey.

Excellent Credit Score

An excellent credit score ranges from 800 to 850. With this score, you get the best interest rates. You also have more negotiating power. It shows you have a strong history of managing debt well.

Very Good Credit Score

A very good credit score falls between 740 and 799. This score offers favorable loan terms. You are seen as a low-risk borrower. You still enjoy competitive interest rates.

Good Credit Score

Good credit scores range from 670 to 739. Most lenders view this score positively. You can qualify for decent interest rates. The loan process is usually smooth with this score.

Fair Credit Score

Fair credit scores range between 580 and 669. Lenders may offer higher interest rates. You might face stricter loan terms. Improving your score can help in the future.

Poor Credit Score

Poor credit scores are 579 and below. This score can make getting a loan difficult. You may face very high interest rates. It’s wise to work on improving your credit score. This opens up better loan options.

Ideal Credit Score For Car Purchase

A credit score of 700 or above is often considered ideal for buying a car. This score can help you secure better interest rates and loan terms. Aim for a score in this range to increase your chances of approval.

When you’re thinking about buying a car, your credit score is a crucial factor that can impact your financing options. But what exactly is an ideal credit score for purchasing a vehicle? Understanding this can help you secure a better deal and save money in the long run. Let’s dive into what makes a good credit score for car purchases.Understanding Credit Score Ranges

Credit scores generally range from 300 to 850. Scores above 700 are considered good and can help you get better interest rates. If your score is above 750, you’re in excellent territory, which can open up the best financing options.Why A Higher Credit Score Matters

A higher credit score can lower your interest rate, potentially saving you thousands over the life of the loan. For example, a person with a score of 750 may receive a rate of 3%, while a score of 600 could result in a rate of 7%. This difference in interest rates can significantly affect monthly payments and total loan cost.What Lenders Look For

Lenders not only look at your credit score but also your credit history. They consider factors like payment history, outstanding debt, and the length of your credit history. Demonstrating a strong history of on-time payments can boost your chances of approval.How To Improve Your Score

If your score needs a boost, start by paying bills on time and reducing existing debt. Regularly check your credit report for errors and dispute any inaccuracies. Simple actions like these can gradually improve your score, making it easier to get a car loan.Is A Co-signer An Option?

If your credit score isn’t ideal, consider using a co-signer to help secure better terms. A co-signer with a strong credit profile can help you qualify for lower interest rates. However, it’s important to remember that your co-signer is equally responsible for the loan.Your Personal Finance Strategy

Think about how a car payment fits into your monthly budget. While it’s tempting to stretch for a more expensive car, sticking to a budget ensures you won’t overextend financially. Consider using online calculators to determine what monthly payments you can comfortably afford. Understanding these elements can transform your car-buying experience. How might focusing on these factors change your approach to purchasing a vehicle?

Credit: www.youtube.com

Impact Of Low Credit Scores

Understanding the impact of low credit scores is crucial when buying a car. A low credit score can make purchasing a vehicle challenging. Many lenders see low scores as risky. This can lead to higher interest rates or even loan denial.

High Interest Rates

Low credit scores often mean higher interest rates on car loans. Lenders charge more to cover potential risks. This can significantly increase monthly payments. Over time, you’ll pay more for the car than someone with a higher score.

Limited Loan Options

Low credit scores limit your loan options. Many banks and lenders prefer clients with good credit. You might have to turn to alternative lenders. These lenders may offer less favorable terms.

Larger Down Payments

With a low credit score, lenders might require larger down payments. This reduces their risk if you default. It can be challenging to save a large sum upfront. This can delay your car purchase.

Potential Loan Denial

Low scores can lead to outright loan denial. Some lenders won’t approve loans for low-credit individuals. You may need to improve your score before trying again. This can be frustrating and time-consuming.

Impact On Car Selection

Low credit can limit your car choices. You might have to settle for a less expensive model. This can affect your satisfaction and needs. A reliable vehicle is important for everyday tasks.

Improving Your Credit Score

A good credit score to buy a car usually ranges from 650 to 750. Scores in this range can help secure better interest rates. Keep track of your credit report to maintain or improve your score for future purchases.

Improving your credit score can make buying a car easier. A higher credit score means lower interest rates. This saves money over time. Here are some simple ways to boost your credit score.Timely Payments

Pay your bills on time, every time. Late payments hurt your credit score. Set reminders or automate payments. This helps maintain a good payment history.Reducing Debt

Lower your total debt to improve your credit score. Focus on high-interest debts first. Pay more than the minimum amount if possible. Keep credit card balances low.Correcting Credit Report Errors

Check your credit report for mistakes. Errors can lower your score unfairly. Dispute any incorrect information. Contact the credit bureau to fix these errors. A clean report helps your score.

Credit: www.badcredit.org

Alternatives For Low Credit Scores

Having a low credit score can be a barrier when trying to buy a car. But don’t let it discourage you. There are several alternatives to help you drive away in your new vehicle even with less-than-perfect credit. Let’s explore some practical options that could work for you.

Co-signers

A co-signer can be your ticket to a better auto loan deal. By having someone with a strong credit score sign the loan with you, lenders see less risk. This might translate to lower interest rates and better terms.

Think of a trusted friend or family member who believes in your ability to make payments. Having their support can improve your chances significantly. But remember, their credit is on the line too, so make sure you’re committed to timely payments.

Buy Here, Pay Here Dealerships

Buy Here, Pay Here (BHPH) dealerships offer a unique solution. They often cater to buyers with poor credit by providing in-house financing.

These dealerships make the process straightforward as they don’t rely on outside lenders. However, keep an eye on potential downsides like higher interest rates. Is the convenience worth the cost? It’s a question worth considering.

Credit Unions

Credit unions could be your hidden gem in finding a car loan with a low credit score. They often provide more personalized service and might be more willing to work with you than traditional banks.

If you’re already a member, or can join one, you might access lower rates and flexible terms. These benefits can make credit unions an attractive option.

Explore the possibility of pre-approval to strengthen your negotiating power with dealers. Is there a local credit union that could offer you a better deal?

These options show that a low credit score doesn’t have to stand in the way of buying a car. By considering alternatives like co-signers, BHPH dealerships, and credit unions, you can find a path that suits your financial situation. Which option aligns best with your needs?

Monitoring Your Credit Score

A credit score of 661 or higher is often considered good for buying a car. It increases your chances of getting better loan terms. Regularly monitoring your credit score can help you plan your car purchase effectively.

Monitoring your credit score is crucial when planning to buy a car. A good credit score can unlock better loan terms and lower interest rates. Keeping an eye on your credit score helps you understand your financial health. It allows you to catch errors and address them promptly. Regular monitoring can also protect you from identity theft. Here’s how you can effectively keep track of your credit score.Understand The Importance Of Regular Checks

Check your credit score regularly to stay informed. It helps you spot discrepancies early. This can prevent unwanted surprises when applying for a car loan.Use Reliable Credit Monitoring Tools

Choose a trustworthy credit monitoring tool. Many services offer free updates on your score. They also send alerts for significant changes.Review Your Credit Report Annually

Get a free annual credit report from each major bureau. Review it for errors or outdated information. Dispute any inaccuracies immediately.Set Up Alerts For Score Changes

Set up alerts to notify you of changes in your credit score. These alerts can help you act quickly if something seems amiss.Understand The Factors Affecting Your Score

Learn what impacts your credit score. Payment history, credit utilization, and account age play significant roles. Knowing these can help you manage your score better.Keep Your Information Secure

Protect your personal information to prevent identity theft. Use strong passwords and monitor your accounts for suspicious activity. Monitoring your credit score doesn’t have to be complicated. With the right tools and habits, you can maintain a strong financial profile.

Credit: m.facebook.com

Frequently Asked Questions

What Is A Decent Credit Score To Buy A Car?

A decent credit score to buy a car typically ranges from 661 to 780. Scores in this range qualify you for favorable loan terms and interest rates. Lenders prefer higher scores, so aim for the best possible to secure better deals.

Can I Get A Car With A 600 Credit Score?

Yes, you can get a car with a 600 credit score. Lenders might offer higher interest rates. Shop around and compare options. Consider saving for a larger down payment to improve loan terms.

What Credit Score Do You Need To Buy A $30,000 Car?

A credit score of 620 or higher is generally required to buy a $30,000 car. Lenders prefer scores above 700 for better interest rates. Check with your lender as requirements can vary. Improving your score can increase financing options and reduce costs.

What Credit Score Do You Need To Get A $30,000 Loan?

A credit score of 600 or higher is typically needed for a $30,000 loan. Lenders prefer higher scores for better terms. Scores above 700 improve your chances of approval and lower interest rates. Always check with specific lenders for their requirements.

Conclusion

A good credit score opens doors to better car loan deals. It helps you save money and get favorable terms. Aim for a score above 670 for better options. This score shows lenders your reliability. It can lead to lower interest rates.

Remember, improving your score takes time. Pay bills on time and reduce debt. Check your credit report regularly. Make informed decisions. A strong credit score makes car buying easier. It helps you enjoy the process, not stress over it. Keep your credit healthy for future needs.

Your car purchase is just the beginning.